Help your clients control their workers’ comp costs with this checklist

- Workers’ compensation premiums are driven by experience ratings. Learn what they are and their effect.

- Basically, fewer claims can mean lower premiums. Your clients can achieve this with a well-articulated safety program.

- Share these essential safety program elements to help clients get started on their loss control programs.

No doubt you as a workers’ compensation insurance agent often are asked by your clients, “How can I control my insurance costs?” And you reply, “The key to controlling your costs is you and your safety program: the safety training you provide and the safety habits your workers absorb and follow, improving your loss prevention.

Related: Top 13 preventable workplace injuries [infographic]

It might help to explain to your clients how experience ratings work and how they can affect them. As you know, each state establishes “manual rates” for employers in various types of businesses. The manual rate is the cost of insurance, per $100 of payroll, for that particular business. A manual rate involves many calculations; one of these is experience rating. As the NCCI (National Council on Compensation Insurance) in their booklet, ABCs of Revised Experience Rating, explains that experience rating is

… a method for tailoring the cost of insurance to the characteristics of an employer. It gives an employer the incentive to manage its own expenses through measurable and meaningful cost-saving safety programs.

Experience rating recognizes the differences among qualifying employers with respect to safety and loss prevention. It does this by comparing the experience of individual employers with the average employer in the same classification. The differences are reflected by an experience rating modification (mod), based on individual payroll and loss records, which may result in an increase, decrease, or no change in premium.

The bottom line: fewer claims can mean lower premiums. Your clients can achieve this with a well-articulated safety program.

Related: Help your work comp clients create a job hazard analysis [Infographic]

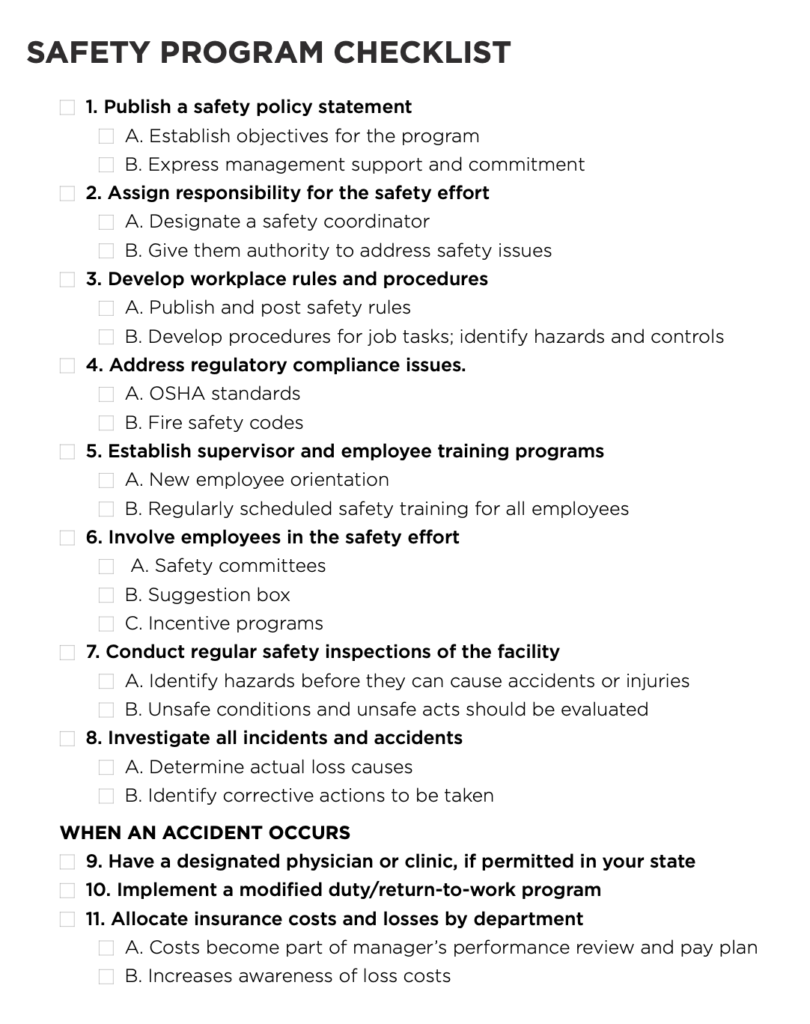

Essential safety program elements

Then your client asks, What are the essential elements of a good safety program? Are some elements more important than others? What’s the quickest and most efficient way to implement a loss prevention program?

Provide this checklist to your workers’ compensation clients to encourage them to establish their safety program.

You can download the checklist here and share it with your work comp clients.

Agents, take a look at our Workers’ Compensation Program to add to your portfolio of insurance solutions.