Key P&C insights and rate forecasts for Q2 2025

This Property & Casualty market trends and forecasts report is courtesy of Brown & Brown Insurance Services, Inc.

Rates continue to shift across commercial insurance — but not always in the same direction. While property rates are beginning to ease in some areas, liability lines are still feeling the pressure of rising claim costs and evolving risks.

Here’s a quick look at key Property & Casualty trends and forecasts shaping Q2 2025, and what producers should watch for in the months ahead:

- Property rates are expected to continue to soften throughout 2025.

- General Liability is estimated to see rate increases of 5-10%.

- Increases in Auto Liability rates are estimated at 7.5-15%.

- Umbrella/Excess Liability is looking at the possibility of a 10-20% increase.

Read on for a deeper dive into what’s driving these forecasts, plus underwriting considerations to keep in mind.

Related: The insurance trends shaping the year

Property

The commercial property insurance marketplace is seeing further stabilization as rates and inflation continue to moderate.

Property rates continue to soften compared to prior years and are expected to continue through 2025. So far, there’s been slightly higher softening than anticipated on favorable accounts. This enhanced competition has benefited many, providing welcome relief from prior terms. It’s possible this trend could continue to develop.

through 2025. So far, there’s been slightly higher softening than anticipated on favorable accounts. This enhanced competition has benefited many, providing welcome relief from prior terms. It’s possible this trend could continue to develop.

Single carrier placements are experiencing slightly different results than shared and layered placements. More benign single carrier placements are experiencing rate changes averaging from +5% to -10%, while layered or shared placements are experiencing +5% to -25%.

Impacts of natural disasters: Accounts in natural disaster-prone geographies, especially in hard-hit industries or severe convective storm locations, have continued to see premium increases, and continued growth will further enhance reserves. In contrast, those in geographies less prone to natural disasters have had higher bargaining power.

Impacts of wildfires: Most of the wildfire losses appear to directly impact the personal lines sector, less so the commercial lines sector. We expect the short-term impact to affect the personal sector, and anticipate properties located in wildfire-prone areas to experience retention at renewal.

Underwriting trends & increased competition: So far in 2025, carriers have continued to be practical regarding their underwriting guidelines as property carriers have pursued more growth and capacity. Competition has risen, especially on accounts with good loss prevention programs, lower natural catastrophe exposures and a favorable loss history.

Related: Why niche products are your key to growth in 2025

Casualty

From rising medical costs to nuclear verdicts, casualty lines continue to face upward pressure — prompting carriers to tighten underwriting, adjust rates and scrutinize risks more closely.

General Liability

Social inflation, litigation financing, regulatory changes and nuclear verdicts are driving rate increases, estimated at 5-10%. Carriers have increased focus on premises liability (assault & battery, sexual abuse and molestation and human trafficking), with underwriters specifically focusing on Real Estate and Habitational Accounts.

Workers’ Compensation

Middle-market workers’ compensation results remain stable to favorable, with  growing concern that emerging trends could become problematic later this year, resulting in potential rate increases. The current market trend is seeing -5% to flat rates for low loss risks and a 5%-8%+ rate for unfavorable loss histories and severe risks.

growing concern that emerging trends could become problematic later this year, resulting in potential rate increases. The current market trend is seeing -5% to flat rates for low loss risks and a 5%-8%+ rate for unfavorable loss histories and severe risks.

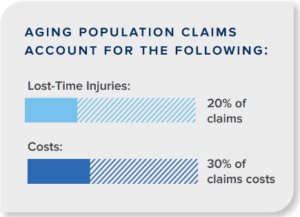

Carriers remain concerned about issues such as opioid use, mental  healthcare and workplace violence. However, the most prominent focus is on how the aging population directly affects claim costs. Claims associated with an aging population account for over 20% of lost-time injuries and over 30% of costs. Another concern is the cost of prescription drugs and the rising cost of hospital and physician services, which continue to rise, driving up the cost of workers’ compensation claims.

healthcare and workplace violence. However, the most prominent focus is on how the aging population directly affects claim costs. Claims associated with an aging population account for over 20% of lost-time injuries and over 30% of costs. Another concern is the cost of prescription drugs and the rising cost of hospital and physician services, which continue to rise, driving up the cost of workers’ compensation claims.

In March 2024, the Department of Labor revised a rule regarding classifying independent contractors as employees under the Fair Labor Standards Act (FLSA). This legislation faces challenges, and an unfavorable outcome could cause greater emphasis on underwriting and additional rates until the marketplace truly understands the impact on the industry

Auto Liability

The U.S. commercial auto insurance market is navigating a complex landscape characterized by escalating costs, evolving risks and technological advancements. Rate increases over the last 10 years have impacted the auto market, yet carriers still struggle with poor loss ratios. Anticipated rate increases range between 7.5-15%. The following factors have impacted auto pricing:

- Nuclear verdicts

- Inflation

- Distracted driving

- Increased scrutiny on hired and non-owned exposure

Producers, be proactive to ensure driver safety handbooks are up-to-date for any employee driving for company businesses.

Umbrella/Excess Liability

Carriers in the excess liability space continue to reduce capacity and look to attach higher limits. Rate increases are anticipated between 10-20%. Inadequate reserves, larger jury awards, nuclear verdicts and litigation funding are the primary causes driving this trend.

Executive Liability

While many of the trends in the executive liability market remain consistent with the previous quarter, the political and economic landscape changes provide some uncertainty. Carriers and underwriters continue to monitor these political and financial developments and their potential impacts.

Tariffs and supply chain disruptions will likely impact inflation and litigation costs. Companies facing financial pressures, historically increase claims exposures as a byproduct of cost-cutting strategies. Additionally, as companies choose to pivot away from diversity, equity and inclusion (DEI) initiatives and programs, there are increased exposures in the employment practice liability (EPL) space.

Need help navigating Q2’s Property & Casualty trends and forecasts?

As market conditions continue to evolve, staying connected with your underwriter is the best way to navigate shifting rates and appetite. Find your program underwriter here.